Credit refers to an agreement to buy goods or services with the promise to pay for it later, with interest.

The interest part means that you will be paying back more money than you borrowed. Owing money can be a stressful part of life, so learning how to manage credit and avoid debt traps can help you be stress-free.

Want to learn how to manage your credit? Check out our 14 steps:

It is always better to buy things with cash, but, if you must use credit, make sure that it is good credit and not bad credit. Good credit is for something that gains value such as starting a business, while bad credit is for something that loses value such as buying new shoes.

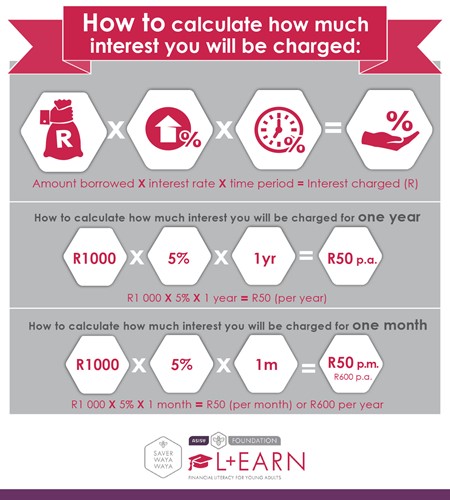

Interest is the extra money the lender charges you to borrow money from them. If you borrow money, you pay interest BUT if you save or invest the money, you earn interest.

Interest is the extra money the lender charges you to borrow money from them. If you borrow money, you pay interest BUT if you save or invest the money, you earn interest.

When you borrow money you need to look at the TOTAL cost you will be paying, which includes the price of the product or service, the interest, and any administrative fees. Only once you know the total cost that you will be paying, can you see whether you can afford it.

Watch this video on how interest works :

TOP TIP: Use these interest calculators to help you work out the total cost of things.

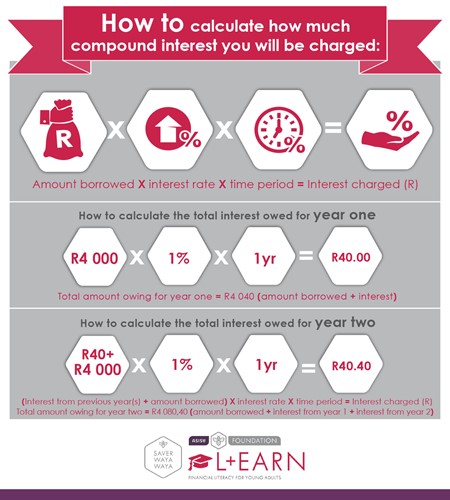

There are two types of interest: simple interest and compound interest

With simple interest, interest is added on the capital amount borrowed or invested only. With compound interest, interest is added on the capital amount borrowed or invested, plus on interest already earned or already owing form previous months or previous periods.

REMEMBER: If you are investing, then you earn interest.

If you are credit active, then you will have a credit profile. This is a record of how well you pay your credit and accounts.

It’s important to have a good credit profile as this shows you are financially responsible and means you will be able to access credit at competitive rates and on reasonable terms.

To get a good credit profile, do these things:

Want to learn more about credit management?

We have some helpful radio clips about this topic with key tips about how to tell the difference between “good” and “bad” credit: click here to listen to them.

Check out the recording of our credit and debt webinar to learn even more about this important financial topic here

Do you want to buy a car one day? If you do you will need to buy it using car finance (a form of credit). Car finance contracts are normally repaid over 48 months (4 years) or 60 months (5 years).

The kind of car you can afford will depend on your living expenses, so before taking out car finance take an honest looking at your monthly living expenses and how much you are left with and if you will be able to afford the repayments for the next 4 – 5 years.

You must also consider what it will cost you to run your car including maintenance, insurance and the ever rising cost of petrol. Stop and think about if you can truly afford a car.

Balloon payments or residual payments basically means you rent or lease a car by making monthly repayments and then at the end of the repayment period if you want to own the car you will need to pay an additional lump sum amount.

The lump sum owed can be as high as 30% of the value of the car. Interest is charged on this lump sum from the beginning of the loan.

For example, if a car was valued at R200,000 and there is a balloon option of 25%, which means that when the loan agreement ends you would be liable for a lump sum of R50,000. Interest would usually be charged on this R50 000. This means that the monthly payments would cover the R150 000, and the R50 000 is paid at the end of the loan term.

If you don’t pay the lump sum the car is taken away by the financier.

If you take out credit you may want to consider taking credit life cover or insurance. This is insurance that will pay your debt if you die, become disabled or become unemployed.

Some credit providers will expect you to take out credit life cover when you take out a loan or credit but you can choose your own credit life cover provider.

If you choose to take out credit life insurance the benefit may be paid in a lump sum or as monthly instalments and your pay out will decrease as your outstanding loan amount decreases.

Once your debt has been repaid your credit life cover ends.

For more information on credit life insurance click here.